As a young physician fresh out of medical school or in the early years of residency, navigating the world of personal finance can be as challenging as a night in the ER.

With significant student loan debt and a delayed entry into earning, establishing a solid financial base early in your career is crucial. This guide aims to assist you in effectively managing your finances, paving the way for a future of financial security. It covers various financial topics, from debt management to investment strategies, as a foundational “Finance for Doctors 101.”

While it provides a comprehensive overview to kickstart your financial literacy journey, it’s important to remember that personal finance is complex and unique to each individual. Therefore, you should conduct your own due diligence and consider consulting a financial professional to tailor these strategies to your specific circumstances. This guide lays the groundwork, but your personal financial journey will require continuous learning, adaptation, and informed decision-making that evolves alongside your medical career.

The Importance of Understanding Finance for Doctors

Why is financial literacy a must for doctors? The statistics can be startling. A significant number of medical professionals find themselves facing financial challenges due to a lack of proper financial planning. For instance, despite high earning potential, doctors often struggle with substantial debt loads, with the average medical school debt exceeding $200,000. Additionally, studies show that many physicians are not adequately prepared for retirement, with some even postponing retirement due to financial constraints.

This article intends to change that narrative and set you up for financial success. By understanding finance principles, you can avoid common pitfalls and make informed decisions that lead to financial stability and independence.

My goal is to provide you with the tools and insights needed for smart financial planning. By boosting your financial knowledge, you’ll be able to focus on your medical career free from financial stress.

Finance for Doctors 101: Navigating Your Financial Health with Confidence

Understanding Your Financial Position

Let’s start by figuring out where you’re at regarding money. This section helps you assess your current financial status, identifying your strengths and areas for improvement.

1. Assessing Student Loan Debt

- Your Total Debt Burden: Start by getting a clear picture of how much you owe in student loans. This includes knowing the total amount, understanding the interest rates, and being aware of the terms of each loan. This clarity is the first step in creating an effective repayment strategy.

- Repayment Plans: Explore Income-Driven Repayment (IDR) plans like Pay As You Earn (PAYE) or Saving on a Valuable Education (SAVE) Plan (formerly the REPAYE Plan), which adjusts monthly payments based on your income. This can be particularly beneficial if you’re starting with a lower salary.

- Loan Forgiveness Programs: If you have federal Direct Loans and are working in a non-profit or government setting, consider the Public Service Loan Forgiveness (PSLF) program. After 120 qualifying student loan payments, your remaining debt could be forgiven tax-free.

- State-Specific Programs: Many states have loan forgiveness programs for medical professionals who work in underserved areas. The terms and benefits vary, so it’s worth researching what’s available in your state.

Example: Suppose you have $200,000 in student loans at an average interest rate of 6.8%. Opting for an IDR plan makes your monthly payments more manageable on a resident’s salary. If you plan to work in a non-profit hospital, you might be eligible for PSLF, leading to significant savings in the long run.

2. Evaluating Current Income and Expenses

- Creating a Budget: Utilize budgeting tools to track your income and expenses. This will help you allocate your income efficiently and effectively across various categories such as housing, food, transportation, loans, and savings.

- Identifying Saving Opportunities: Examine your spending habits for areas to cut back, like cooking at home instead of dining out, opting for more affordable housing, or purchasing a used vehicle.

- Balancing Needs and Wants: Distinguish between essential and discretionary spending. Aim to reduce non-essential expenses, particularly in areas that don’t significantly enhance your quality of life. Be wary of lifestyle creep — the tendency to increase spending as income rises. Staying vigilant against this habit can help you maintain financial discipline, ensuring that your increased earnings contribute to savings and investments rather than just higher expenses.

Example: If you bring lunch to work instead of eating out, you could save around $200 a month. You can channel this extra amount to your emergency savings or accelerate your loan repayments.

3. Understanding Credit Management

- Achieving a High Credit Score: A strong credit score is essential for financial health. It affects your ability to obtain loans and secure favorable interest rates for big purchases like a new car or home. Prioritize building and maintaining a high credit score as part of your financial strategy.

- Paying Bills on Time: One of the simplest ways to maintain a good credit score is by paying your bills on time. Consider setting up automatic payments to ensure you never miss a due date, as late payments can significantly harm your credit score.

- Keeping Credit Card Balances Low: Be prudent with credit card usage. Aim to spend within your means and use less than 30% of your available credit limit. Keeping your credit utilization low can help improve your credit score.

- Regularly Monitoring Credit Reports: Review your credit reports for inaccuracies or fraud. Correcting any errors you find is crucial in maintaining an accurate and robust credit score.

Example: You can use a credit card for everyday purchases and pay off the balance in full each month. This strategy keeps your credit utilization low and builds a positive credit history, which is beneficial for future financial endeavors like securing a mortgage.

By actively managing your student loans, budgeting wisely, and maintaining a healthy credit profile, you can establish a solid financial foundation early in your medical career, setting the stage for long-term financial success.

Budgeting and Saving

Next, let’s dive deeper into how to budget and save effectively. It’s all about making your money work for you, ensuring you can enjoy life while securing your financial future.

1. Budgeting Techniques

- 50/30/20 Rule: Familiarize yourself with different budgeting techniques. For instance, the 50/30/20 rule is a simple yet effective budgeting framework that can help manage your finances. It divides your income into three categories: 50% for necessities like rent and groceries, 30% for discretionary spending such as hobbies and dining out, and 20% for savings and debt repayment. It’s an effective way to manage your money, ensuring you cover essential expenses while saving and enjoying some of your earnings.

- Zero-Based Budgeting: In zero-based budgeting, you assign every dollar of your income to specific expenses, savings, or debt payments, aiming for zero unallocated funds by the month’s end. This method is detailed and disciplined, helping to prevent overspending and ensuring your money is being used effectively towards your financial goals.

- The Envelope System: The envelope system divides your cash into envelopes for different spending categories, like groceries and entertainment. Once you use up the money in an envelope, you stop spending in that category until it’s refilled. This tangible approach helps manage spending and is especially effective for controlling discretionary expenses.

- Implementation: Start by tracking your monthly expenses to understand where your money goes and to get a clear picture of your cash flow. Then, choose a budgeting method that suits your financial situation and lifestyle. For example, if you prefer a more structured approach, the zero-based budget might be ideal for you.

Example: The 50/30/20 rule can be quite effective on a resident’s budget. Allocate 50% of your income to essentials like rent and loan payments, 30% to lifestyle expenses, and 20% to savings and loan repayments. Utilize free meals in the doctor’s lounge to boost your savings, allowing you to reallocate dining funds for celebrating milestones or additional savings.

2. Emergency Savings

- Setting a Target: Strive to save at least three to six months of living expenses. This fund provides a cushion for unforeseen circumstances like job loss, unexpected medical bills, or urgent travel.

- Building the Fund: Start small if necessary and gradually increase your contributions. Setting aside a percentage of each paycheck can build up over time. Consider opening a high-yield savings account specifically for this purpose, where your money can earn interest.

Example: If your monthly expenses amount to $3,000, aim for an emergency fund between $9,000 to $18,000. You could start by saving $200 from each paycheck, gradually increasing the amount as your salary grows or your debts decrease.

3. Short-term vs. Long-term Savings Goals

- Balancing Goals: While saving for immediate needs is essential, also focus on long-term objectives. This may include saving for a down payment on a house, investing in retirement accounts, or setting aside funds for your children’s education.

- Strategies for Goal Setting: Prioritize your goals based on their importance and timeline. Consider liquid savings options like savings accounts or short-term investments for short-term goals. Consider retirement accounts (IRA, 401(k)), stocks, index funds, or mutual funds for long-term goals.

Example: You might allocate some of your income to a down payment fund for a home you plan to buy in five years. Simultaneously, contribute to a retirement account like a Roth IRA to take advantage of compound interest over time.

By implementing these budgeting and saving strategies, you effectively manage your current financial situation and pave the way for a more secure financial future. Remember, financial planning is a dynamic process, and it’s essential to periodically review and adjust your budget and savings goals as your circumstances evolve.

Investing Basics for Physicians

Now, let’s talk about growing your wealth. This part covers the basics of investing, tailored for physicians to help you confidently navigate the investment world.

1. Understanding Investing

- Diversification: A fundamental principle in investment is diversification, which involves spreading your investments across various assets to manage risk. Your portfolio should ideally include a mix of stocks, bonds, and cash.

Stocks, or shares in companies, offer the potential for high returns but come with higher risks. Bonds, essentially loans to companies or governments, typically offer lower returns but are generally less risky. You should also include cash in your portfolio. Cash provides liquidity and stability, acting as a buffer during market volatility. It ensures immediate access to funds when needed, whether for emergency expenses or taking advantage of new investment opportunities.

- Starting Small: You don’t need much capital to begin investing. You can start small, using robo-advisors or online investment platforms, which allow you to invest with minimal initial capital. These platforms often offer the ability to create a diversified portfolio that aligns with your risk tolerance and financial goals, including the appropriate mix of stocks, bonds, and cash.

- The Advantage of Starting Early: Investing early in your career can have significant long-term benefits. Early investments have more time to grow through the power of compound interest, potentially leading to substantial wealth accumulation over time. This early start can be particularly impactful for retirement savings, giving your investments more time to grow and compound before you need to access them.

Example: If you invest $1,000 at age 30 with an annual rate of return of 8%, by the time you reach age 65, that investment would grow to approximately $14,785. This calculation demonstrates the power of compound interest over time.

2. Risk Management

- Assessing Risk Tolerance: Determine your risk tolerance based on financial goals, investment timeline, and emotional comfort with market fluctuations. As a young physician, you likely have a longer time horizon for investing, which generally allows you to take on more risk.

- Regularly Reviewing and Adjusting: Regularly review and adjust your investment portfolio. As you get closer to retirement or your financial goals change, you may want to shift towards more conservative investments to ensure a more dependable flow of income.

Example: If the thought of market downturns keeps you up at night, consider a more conservative portfolio with a higher percentage of bonds. On the other hand, a stock-heavy portfolio might be more suitable if you’re comfortable with short-term market fluctuations for potentially higher returns.

3. Retirement Planning

- Investing in a Retirement Account: Familiarize yourself with different types of retirement account to optimize your retirement savings. Private practice groups typically offer a 401(k), commonly accompanied by employer matching contributions. Academic centers often provide a 403(b) plan tailored for employees in the educational and non-profit sectors. Non-profit hospitals may offer a 457 plan, which features deferred compensation benefits. If you work for the Veterans Administration (VA), you may be eligible for the Federal Employees Retirement System (FERS), a retirement plan unique to federal employees.

For personal retirement savings, consider an Individual Retirement Account (IRA), which comes in two main types: Traditional and Roth IRAs, each with distinct tax advantages.

Each account type – 401(k), 403(b), 457, FERS, and IRA – has its own rules and benefits. Make sure to learn what they are!

- Maximizing Employer Match: If your employer offers a 401(k) match, try to contribute at least enough to get the full match. This is essentially free money and a significant boost to your retirement savings.

- Considering Target Date Funds: Opting for a target date fund within your retirement account can be an ideal choice for those seeking a low-maintenance approach to retirement savings. These funds dynamically modify their investment mix as you approach your retirement age.

Initially, they might invest more heavily in stocks for growth potential, but as your retirement date nears, the fund gradually shifts towards more conservative assets like bonds, aiming to preserve capital. This built-in adjustment mechanism ensures that your investment strategy aligns with your changing risk tolerance over time, offering a hassle-free solution to achieving a balanced and age-appropriate investment portfolio.

You can “set it and forget it” with a target date fund. Of course, it’s wise to periodically review your investment to ensure it continues to align with your overall financial goals and changing life circumstances.

Example: If your employer matches 50% of your 401(k) contributions up to 6% of your salary and you earn $100,000 annually, you should aim to contribute at least $6,000 annually to maximize this benefit. Your employer would then add $3,000.

Understanding and engaging in these investment strategies can build wealth over time. It’s important to remember that investing is not a one-time task but a continuous process that should evolve with your changing financial circumstances and goals. As a physician with a demanding career, considering the services of a financial advisor might also be beneficial to help manage and optimize your investment strategy.

Insurance Needs for Physicians

Insurance is vital to protecting your hard-earned assets. Here, you’ll learn about the types of insurance you should consider to safeguard both your professional and personal life.

1. Professional Insurance: Malpractice Insurance

- Understanding Malpractice Insurance: As a physician, malpractice insurance is essential to protect yourself against legal claims regarding your medical practice. There are two main types: claims-made and occurrence policies. Understanding the difference between claims-made and occurrence policies is crucial.

Claims-made policies provide coverage for claims filed during the policy’s active period. This means that if a claim is made against you, it will only be covered if the policy is in effect both when the incident occurred and when the claim is filed. It’s important to note that once a claims-made policy lapses or is canceled, no coverage exists for claims filed afterward, even if the incident occurred while the policy was active. This is where tail coverage becomes essential as it extends the period when a claim can be made.

On the other hand, occurrence policies offer a more comprehensive coverage approach. They cover any incident that occurs during the policy’s period, regardless of when the claim is made. This means that if an incident happened while the occurrence policy was active, you’re covered for any future claim related to that incident, even if the policy is no longer in effect. Occurrence policies provide more lasting peace of mind since they don’t require additional tail coverage. However, they might come with higher premiums than claims-made policies due to their extended coverage.

- Choosing the Right Coverage: Evaluate factors like coverage limits, the extent of coverage, and the insurer’s reputation. It’s also important to understand the policy’s consent-to-settle clause, which dictates whether you have a say in settling a claim.

Example: As a new physician, check if your employer provides malpractice insurance. Should you need to purchase your own policy, consider starting with coverage limits of $1 million per occurrence and $3 million in aggregate, standard starting points.

It’s equally important to assess your need for tail coverage, especially if you opt for a claims-made policy. Tail coverage ensures protection against claims made after your policy ends for incidents that occurred while the policy was active. This is crucial, as medical malpractice claims can sometimes be filed years after the incident.

Adjust your coverage and tail coverage based on the risks associated with your medical specialty and practice location. Ensuring adequate immediate and long-term protection is critical to safeguarding your professional and financial well-being.

2. Personal Insurance: Health, Life, and Disability Insurance

- Health Insurance: Ensure you have a comprehensive health insurance plan, considering factors like coverage, deductibles, co-pays, and network of healthcare providers.

- Life Insurance: Life insurance provides financial protection for your dependents in the event of your untimely death. Term life insurance covers you for a specific term (e.g., 20 years) and is often a cost-effective option for young physicians.

- Disability Insurance: Given the significant investment in your medical training, disability insurance is a great idea. It provides income if you can’t work due to illness or injury. Look for a policy with “own-occupation” coverage, which provides benefits if you can’t perform your specific medical specialty.

Example: You might opt for a term life insurance policy with a death benefit that sufficiently covers any debts and provides financial support for your family’s needs. For disability insurance, selecting a policy that covers at least 60-70% of your income is advisable, with benefits extending until retirement age.

Starting these policies early in your career not only capitalizes on lower premiums due to your age and health but also ensures that you’re covered during the prime years of your career when you and your family may be most financially vulnerable. This proactive approach to insurance planning is crucial in securing your financial future and protecting your loved ones.

3. Umbrella Insurance

- Importance of Umbrella Insurance: This type of insurance provides additional liability coverage beyond what your homeowners or auto insurance policies offer. It can protect your assets and future earnings in case of a lawsuit.

- Determining Coverage Needs: Coverage typically starts at $1 million and goes up depending on your assets and risk exposure. As a physician, your high earning potential and public profile increase your vulnerability to legal claims, making umbrella insurance a key component of your asset protection plan.

Example: If you’re involved in a severe car accident where you are at fault, and the damages exceed your auto insurance liability limits, umbrella insurance can cover the additional costs, protecting your assets and savings.

You can safeguard your career, health, financial stability, and future earnings by thoroughly understanding and obtaining the right mix of professional and personal insurance, including the often-overlooked umbrella insurance. Regularly reviewing and adjusting your insurance coverage to match your changing personal and professional circumstances is crucial to ensuring ongoing protection.

Tax Planning for Young Physicians

Taxes can be tricky, but we’ve got you covered. This section guides you through tax planning strategies to maximize your earnings and minimize your tax liabilities.

1. Basics of Taxation

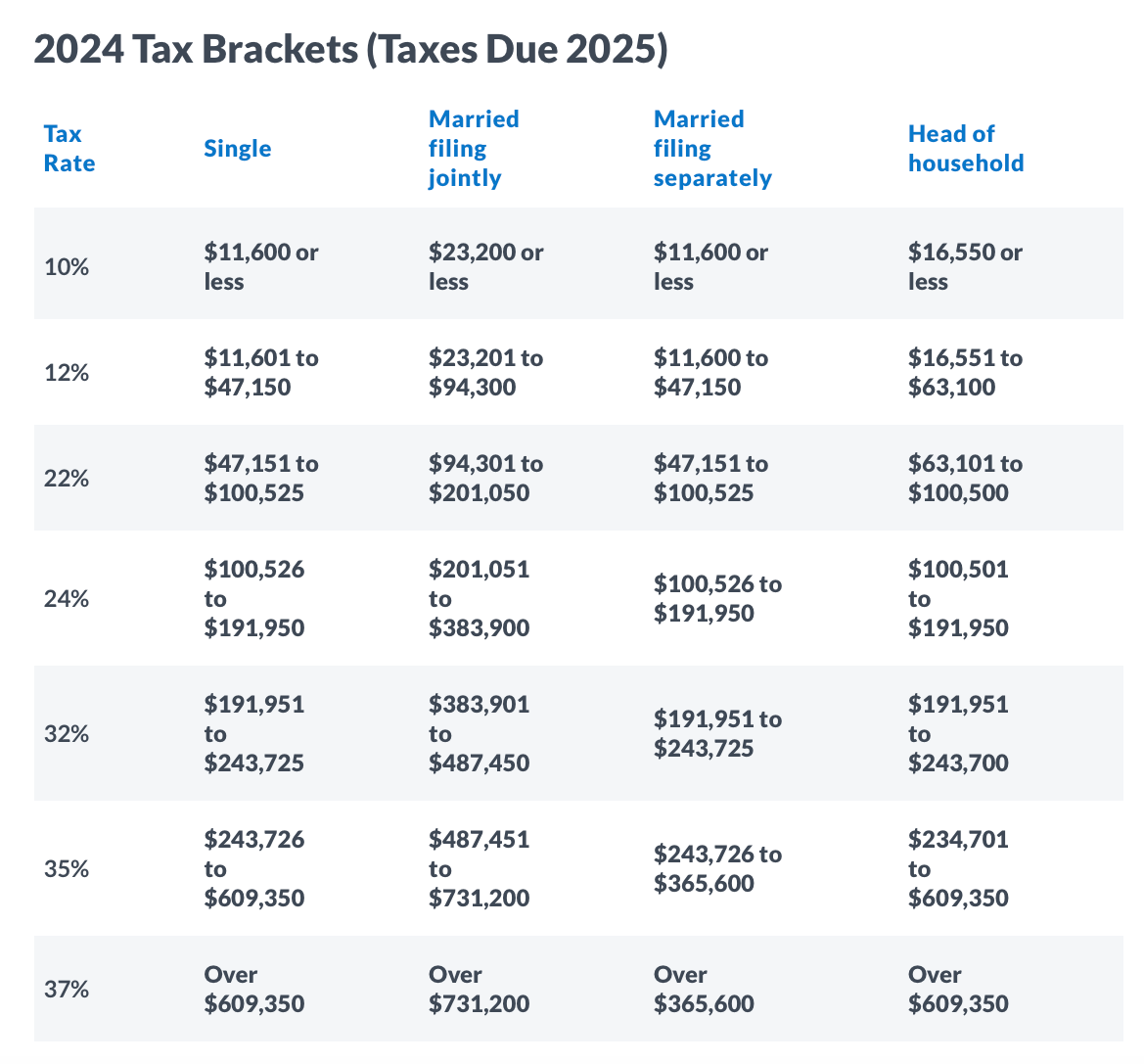

- Understanding Your Tax Bracket: Knowing which federal tax bracket you fall into is crucial for effective tax planning. For 2024, the U.S. federal tax brackets are as follows (these rates apply to taxable income):

- Maximizing Deductions and Credits: Remember the standard deduction, a simple yet effective way to reduce your taxable income when filing taxes. In 2024, the standard deduction amounts to $14,600 for single filers and those married filing separately, $29,200 for joint filers, and $21,900 for heads of household.

Sometimes, itemizing deductions can save you more. You may be able to deduct a range of expenses, including professional expenses, medical equipment purchases, education-related costs, mortgage interest, and more. Itemizing can lead to significant tax savings if your total deductions exceed the standard deduction. Carefully assess your potential deductions to determine whether itemizing is the most beneficial approach for your tax situation.

Example: If your taxable income as a single filer is $100,000, you fall into the 22% tax bracket. However, this doesn’t mean all your income is taxed at 22%. Instead, it’s taxed progressively at the different rates as your income moves through the tax brackets. Based on the 2024 federal tax brackets for a single filer, if your taxable income is $100,000, your federal income tax would be approximately $17,053.

Example #2: If you are in the 22% tax bracket, every $1,000 in deductions can save you $220 in taxes. Eligible deductible expenses include professional fees, medical equipment purchases, costs associated with attending medical conferences, continuing medical education expenses, and home office expenses, if applicable. You can significantly reduce your taxable income by meticulously tracking and claiming all these eligible expenses.

2. Tax-Advantaged Investments

- Health Savings Accounts (HSAs): If you’re generally healthy and want to optimize your healthcare spending, consider enrolling in a high-deductible health plan that allows you to contribute to an HSA. HSAs offer a triple tax advantage: your contributions are tax-deductible, the earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. This makes HSAs an excellent tool for immediate healthcare cost savings and long-term financial planning. Not only do they provide a way to cover current medical expenses, but they also allow you to build a tax-advantaged reserve for future healthcare needs.

- Flexible Spending Accounts (FSAs): FSAs allow you to set aside pre-tax dollars for eligible health care and dependent care expenses, reducing your taxable income. However, it’s important to note that FSAs operate on a ‘use it or lose it’ basis. Any funds not used within the plan year or by the end of any grace period offered by your employer will be forfeited. Therefore, careful planning is essential to estimate your expenses accurately and avoid losing unused funds.

- Understanding Contribution Limits: Be aware of the annual contribution limits for these accounts, as exceeding them can lead to tax penalties. Staying informed about the current year’s limits will help you plan your contributions effectively.

Example: Contributing $3,000 to an HSA, if you’re in the 22% tax bracket, could reduce your tax bill by approximately $660. Similarly, utilizing an FSA for eligible healthcare expenses can offer significant tax savings.

3. Seeking Professional Help

- Complex Tax Situations: As a physician, especially if you have multiple income sources (like investments, rental properties, or side hustles), your tax situation can become quite complex. In such cases, consult with a tax professional.

- Optimizing Tax Strategies: A tax professional can assist in maximizing retirement contributions, understanding the implications of additional income, and planning for significant expenses or investments to optimize your tax situation.

Example: Suppose you’re considering a side job or have rental property income. A tax advisor can guide you in managing these additional income streams in the most tax-efficient manner.

Proper tax planning is key to financial efficiency, especially for young physicians who may face unique financial circumstances due to their profession. Understanding your tax bracket, making the most of tax deductions and credits, utilizing tax-advantaged investment vehicles, and seeking professional guidance are crucial steps in managing your taxes effectively. Regularly updating and reviewing your tax strategy in line with your changing financial situation will ensure you remain on track with your financial goals.

Debt Management and Loan Repayment

Debt doesn’t have to be daunting. Learn practical strategies for managing and repaying your loans, setting you on a path to financial freedom sooner than you might think.

1. Prioritizing Debts

- High-Interest Debts First (Avalanche Method): Tackle debts with the highest interest rates first, typically credit card debts. This strategy, the avalanche method, can save you significant interest over time. However, this method requires substantial discipline as immediate results are usually not very visible.

- Balancing Multiple Debts: If you have multiple debts (student loans, credit cards, car loans), list them by interest rate. Pay more than the minimum on the highest interest debt while maintaining minimum payments on others. Once you pay off the highest interest debt, move to the next.

- Choosing the Right Method for You: While the avalanche method has the best interest-saving benefits, choosing a debt repayment strategy that aligns with your motivation and financial habits is more important. If seeing quick results is more motivating for you, the snowball method of paying off the smallest debt first might be a better fit, even if it means paying more interest over time.

Example: Imagine you have a credit card balance with a 19% interest rate and student loans at 6%. By focusing on paying off the credit card debt first using the avalanche method, you’ll reduce the total interest paid, freeing up more money to tackle the student loans next. However, if you need the motivation of small wins along the way, focus on clearing the smallest debts first (the snowball method).

2. Refinancing Student Loans

- Lowering Interest Rates: If you have private student loans or high-interest federal loans, refinancing can lower your interest rate, reducing the total repayment amount and possibly shortening your repayment period.

- Refinancing Considerations: Be cautious about refinancing federal student loans, as you’ll lose federal benefits like income-driven repayment plans and eligibility for loan forgiveness programs.

Example: Suppose you have private student loans with an 8% interest rate. By refinancing to a lower rate, say 5%, you could save thousands in interest over the life of the loan, assuming the same repayment period.

3. Creating a Repayment Timeline

- Setting Goals and Deadlines: Establishing a clear timeline for your debt repayment can be incredibly motivating. Set realistic goals for when you want to pay off specific debts and create a schedule that aligns with these targets. A timeline helps you visualize the end goal and track your progress, keeping you motivated and focused.

- Adjusting As Needed: Your financial situation can change over time, so it’s important to reassess and adjust your repayment timeline periodically. This might mean accelerating payments when you have extra income or adjusting your goals if faced with unexpected financial challenges.

Example: If you aim to be debt-free in five years, map out a monthly payment plan for each debt. Monitor your progress and celebrate milestones, like when you pay off a particular debt, to maintain momentum and commitment to your overall goal.

You can efficiently navigate toward a debt-free future by strategically managing high-interest debts, utilizing refinancing options, and setting a clear repayment timeline. Remember to periodically review and adjust your strategy in response to any financial changes or goals, ensuring a focused and effective path to financial freedom.

Planning for the Future

Thinking ahead is crucial. This part will explore how to set and achieve your long-term financial goals, ensuring you’re prepared for whatever the future holds.

1. Setting Financial Goals

- Defining Your Goals: Identify your short-term and long-term financial objectives. Short-term goals might involve paying off high-interest debt or saving for a much-needed vacation. In contrast, long-term aspirations could include buying a house, preparing for retirement, or setting up a college fund.

- Creating a Roadmap: Develop a strategy for reaching these goals. This may involve budgeting, setting up automated savings, or making informed investment choices. Calculate the amount you need for each goal and establish a realistic timeline for achieving them.

Example: If you plan to buy a house in five years requiring a $50,000 down payment, figure out your monthly savings target. Consider implementing automatic transfers to a savings or investment account for this purpose.

2. Work-Life Balance

- Prioritizing Your Well-Being: As a physician, the rigors of the profession can often overshadow personal needs. Striking a balance between your personal and professional life is critical for your overall well-being. This balance allows for time spent on hobbies, family, and self-care.

- Implications for Career Longevity and Daily Resilience: A well-balanced life contributes to career sustainability and enhances your ability to handle daily professional demands. It prevents burnout, keeps you mentally and physically healthy, and ensures you remain engaged and adaptable in your career. This balance often involves making choices that favor personal well-being, sometimes even over financial gain, such as opting for a job with more manageable hours or a better lifestyle fit.

Example: You may choose a position in a clinic with regular hours over a higher-paying but more demanding hospital role. While affecting short-term income, this decision can lead to improved mental health, greater job satisfaction, and a sustainable career, enabling you to practice medicine effectively over the long term.

3. Continuous Learning and Adaptation

- Staying Informed and Adaptable: The medical and financial landscapes are ever-evolving. Keep abreast of the latest developments in healthcare, finance, and investments. Be prepared to adjust your financial strategies as your personal and professional circumstances change.

- Seeking Professional Advice: As your financial situation grows in complexity, don’t hesitate to seek advice from financial advisors. This is especially important for significant financial decisions or if your circumstances become more intricate.

Example: Revisit your financial plan as your career progresses and your income increases. This might involve reallocating your increased income towards your existing financial goals or setting new ones.

By setting and diligently working towards your financial goals and maintaining a healthy work-life balance, you lay the foundation for a fulfilling and long-lasting medical career. Financial and career planning are dynamic processes; regularly reviewing and updating your strategies is vital to long-term success and personal fulfillment.

Navigating Financial Considerations Unique to Physicians

Finally, let’s tackle the unique financial considerations you face as a physician. From accepting a contract to choosing between private practice and hospital employment, this section prepares you to make informed and strategic decisions.

1. Contract Negotiation

- Understanding Your Value: Before entering any contract negotiations, research and understand the typical salary and benefits for your position and experience level within your geographic area. This knowledge will give you a solid foundation for negotiation, when possible.

- Negotiating an Employed Position: You have more leeway to negotiate your salary and benefits package in an employed position. Look at the base salary, bonus structures, paid time off, continuing medical education allowances, and retirement plan contributions. Remember, your overall compensation is not just about the salary; benefits play a significant role, too.

- Navigating Partnership Contracts: If you’re considering a partnership in a private practice group, the typical setup includes a pre-partnership phase, usually lasting 1-3 years, where you will likely receive a salary or a percentage of what the partners earn. After this period, you are hopefully voted in as a partner. Note that partnership contracts are often standardized, with all partners having identical contracts. This can make negotiation more challenging than in employed positions, where terms are often more flexible.

- Assessing Contract Terms: Whether negotiating an employed position or understanding the terms of a partnership, ensure you’re clear on all aspects of the contract. In partnerships, pay particular attention to buy-in requirements, profit-sharing, decision-making processes, and the buy-out process.

Example: During contract negotiations for an employed position, you can leverage your unique skills or specialties to justify a higher salary. If the employer can’t meet your salary expectations, which is frequently the case, consider negotiating for additional benefits like a signing bonus, a more favorable bonus structure, tail coverage for claims-made malpractice insurance, or student loan repayment assistance.

2. Strategic Location Choices

- Considering Geographic Factors: Sometimes, the path to financial stability involves making strategic decisions about where to work. If your medical practice allows for the flexibility to choose your work location, consider practicing in less geographically desirable or rural areas that often come with financial incentives like higher salaries or additional benefits. These incentives are offered to attract skilled professionals to areas with higher demand for medical services. Choosing such a location, especially early in your career, can be a smart move for accelerating your financial growth.

- Long-Term Benefits: Committing to a few years in a high-demand area can have significant long-term financial benefits. The higher income and possible bonuses or loan repayment programs can help you aggressively pay down student loans, build your savings, and invest in your future. This financial head start could provide more options later in your career, such as the flexibility to choose a job based on preference rather than financial need or even an earlier retirement.

Example: Opting to work in a less geographically desirable area, you view this as an extension of your residency – a strategic, temporary step in your long-term plan. The lower cost of living, coupled with being more valued in a high-demand setting, not only helps you quickly pay off student loans and boost your savings but also hones your skills and builds confidence. This choice accelerates your path to financial independence while enriching your professional experience.

3. Private Practice vs. Hospital Employment

- Private Practice Pros and Cons: Private practice offers autonomy and the potential for higher earnings, but it also involves managing a business, which includes overhead costs, staffing, billing, and insurance complexities. The financial rewards can be greater, but so are the risks and responsibilities.

- Hospital Employment Pros and Cons: Hospital employment typically offers a more stable income, with set hours and fewer administrative responsibilities. Benefits like health insurance, retirement plans, and malpractice insurance are often part of the package. However, you may have less autonomy in decision-making and limited potential for increased earnings compared to private practice.

Example: If you value stability and a predictable income over the potential for higher earnings and more autonomy, hospital employment might be the better choice for you. On the other hand, if you’re entrepreneurial and willing to take on the challenges of running a business, private practice could offer greater long-term financial and professional rewards.

4. Locum Tenens

- Flexibility and Other Opportunities: Working as a locum tenens physician can offer unique opportunities. This role typically involves temporary assignments in various locations, providing a flexibility that permanent positions may not offer. Working as a locum tenens allows you to gain diverse clinical experiences, broaden your professional network, and explore different healthcare settings. This can be particularly valuable for early-career physicians looking to find their niche or late-career physicians looking for ultimate flexibility or to explore the country.

- Financial Considerations: Locum tenens work often comes with competitive pay rates and, in some cases, additional benefits like housing and travel reimbursements. This can be a strategic way to boost your income, especially if you’re willing to take assignments in underserved or rural areas with high demand for physician services.

Knowing the tax implications of locum tenens work is important, as it often requires managing your taxes as an independent contractor. This includes setting aside a portion of your income for taxes and tracking deductible work-related expenses.

- Weighing Pros and Cons: While locum tenens work can offer flexibility and financial benefits, it also requires adaptability and may involve irregular schedules or periods away from home. Locum tenens may also require obtaining additional state licenses and frequent credentialing for each new job opportunity. Weigh these factors carefully to determine if locum tenens work aligns with your personal and professional goals.

Example: As a recent residency graduate working as locum tenens, you find yourself in rural assignments with competitive pay and perks like housing and travel coverage. This enhances your income and broadens your medical exposure and skillset, building your professional confidence and preferences.

5. Balancing Financial and Professional Goals

- Aligning Choices with Goals: Your decisions should align with both your financial goals and your career aspirations. Consider how each option fits into your overall life plan, including work-life balance, income potential, and professional development.

- Seeking Advice: Consulting with mentors, financial advisors, and colleagues can provide valuable insights into the pros and cons of each path. They can offer advice based on experience and help you weigh your options.

Tip: Talk to other physicians. Understanding their experiences can provide a realistic perspective on what to expect in terms of income, work-life balance, and career satisfaction in each option.

You can align your career with your financial and personal goals by mastering contract negotiation, making strategic location choices, and deciding between private practice, hospital employment, or working as locum tenens. These decisions impact not just your immediate finances but also your long-term career satisfaction and financial stability.

From My Life to Yours: Tips for Lasting Financial Success

I want to offer you some valuable financial advice, some of which I wish I had embraced earlier in my own life. These insights blend lessons learned and wisdom gained, each pivotal in achieving lasting financial success. I hope these tips pave your way to a secure and prosperous financial future.

1. Conquering Student Debt: Aggressive Repayment Tactics

- Extra Payments: Tackle your student loans by making more than the minimum payments whenever possible. This approach can significantly reduce the total interest paid over the life of the loan.

- Interest Rate Update: If dealing with high-interest loans, consider refinancing to secure a lower interest rate, which leads to significant savings over time. However, ensure you understand the terms and conditions of the refinancing to avoid losing any benefits associated with your original loans.

- Alternative Funding Sources: In some situations, exploring alternative funding sources, such as borrowing from family or friends, may be feasible. This approach can offer more favorable terms and a quicker pathway to paying off your loans. Handling such agreements professionally, with clear terms and expectations, is crucial to maintain healthy personal relationships.

2. Tax-Smart Paycheck Planning: Avoiding Year-End Surprises

- Accurate Withholdings: Adjust your tax withholdings to ensure you don’t receive a large bill at tax time. Use tools like the IRS withholding calculator or consult a tax professional to get it right.

- Leverage Tax Deductions for Optimal Savings: A key strategy to minimize taxable income is taking full advantage of tax deductions. Contributing to pre-tax retirement accounts like 401(k)s or IRAs, Health Savings Accounts (HSAs), and Flexible Spending Accounts (FSAs) not only helps in future financial planning but also provides immediate tax relief.

- Deductible Expenses: Be aware of deductible expenses that can lower your tax bill. As a physician, you might have professional deductible expenses such as licensing fees, medical association dues, malpractice insurance premiums, and continuing medical education costs. Maintain thorough records of all these deductible expenses throughout the year. Keep receipts, invoices, and relevant documentation organized and readily accessible for tax filing. This ensures you can accurately claim all eligible deductions.

3. Prioritize Savings: The Pay Yourself First Strategy

- Automated Savings: Set up automatic transfers to your savings or retirement accounts as soon as your paycheck arrives. This habit ensures that saving takes priority in your financial plan.

- Max Out 401(k) Contributions: Maximize your retirement contributions to reduce taxable income and enhance your long-term financial security through compound interest. At the very least, if your employer offers a 401(k) match, contribute enough to get the full match. It’s one of the simplest ways to boost your retirement savings.

4. Smart Investing: The Power of Index Funds

- Realities of Beating the Market: For most investors, consistently outperforming the market is challenging. Statistically, even professional fund managers often struggle to beat major market indices over the long term. As a busy physician, your time and energy are precious resources, and the complexity of active stock investing might not align with your demanding schedule.

- Diversification Made Easy: Index funds present an efficient solution. By investing in a range of companies that mirror a market index, such as the S&P 500, you gain broad exposure to the stock market. This diversification can help mitigate risk, as you’re not reliant on the performance of a single stock or sector.

- Reduced Fees, Increased Returns: The passive nature of index funds means they typically have lower management fees than actively managed funds. Over time, these lower fees can make a significant difference in your investment returns. Moreover, the power of compounding on these savings further enhances your potential for long-term financial growth.

- Time-Efficient Investment Strategy: As a physician, your time is often limited. Index funds offer a more set-and-forget style of investing. Once you’ve selected your funds, minimal ongoing management is required. This hands-off approach is time-efficient and aligns well with the long-term investment horizon needed for substantial growth.

5. Early Sacrifice, Long-Term Gain: Embracing Delayed Gratification

- Avoid Lifestyle Inflation: As tempting as it is to increase your spending with every raise, maintaining a modest lifestyle can accelerate your financial goals, like savings and debt repayment.

- Focus on the Future: Prioritize long-term objectives, such as building a substantial retirement fund or owning your home outright. The sacrifices you make today will reward you with financial freedom and peace of mind down the road.

Implementing these strategies can create a robust financial foundation and allow you to pursue your medical career with the assurance that your finances are on the right track. Each decision you make today is a step towards a future of financial independence and success.

Final Thoughts

Starting your medical career is an exciting time filled with opportunities and challenges. Taking charge of your finances early sets you up for a successful, secure future. Remember, the best time to start planning your financial future is now. Good luck!